World Economic Situation And Prospects: June 2018 Briefing, No. 115

- Global growth expected to reach 3.2 per cent in 2018 and 2019

- Key downside risks to the global economy include rising trade tensions, elevated debt and uncertainty over monetary policy adjustments in the developed countries

- Recent strengthening of economic growth carries environmental costs

English: PDF (175 kb)

Global issues

Global economic prospects continue to strengthen, but risks have increased

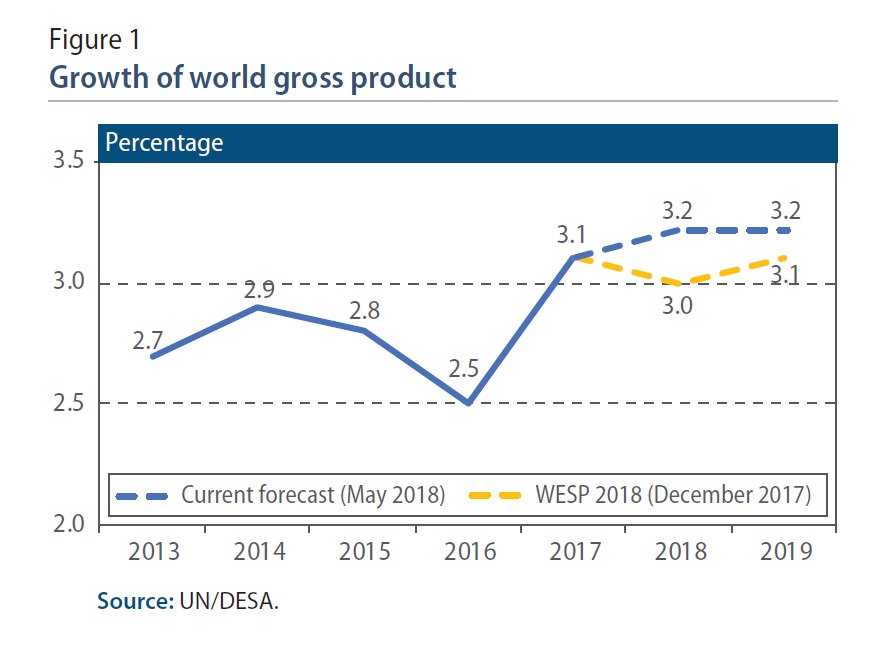

Short-term prospects for the world economy have generally improved over the last six months. According to the World Economic Situation and Prospects as of mid-2018 report, global economic growth is expected to reach 3.2 per cent in both 2018 and 2019, marking an upward revision of 0.2 and 0.1 percentage points compared to forecasts released in December (figure 1). This is the fastest rate of growth since 2011, and reflects upward revisions to forecasts for roughly 40 per cent of the world’s economies. Underpinning this is a stronger outlook for developed economies, reflecting rising wages, favourable investment conditions and the short-term impact of fiscal stimulus measures in the United States. Many commodity-exporting countries are also benefitting from higher prices of energy and metals.

However, alongside the improvement in short-term prospects, downside risks to global growth have also been building. This means that there is a greater probability that economic growth could turn out far worse than current baseline projections. Key risks include the build-up of trade tensions among major economies; increasing geopolitical tensions; greater uncertainty about the path of monetary policy adjustment in developed economies; and high and rising levels of debt in both developed and developing countries. Any of these factors have the potential to derail the recent improvement in economic prospects.

However, alongside the improvement in short-term prospects, downside risks to global growth have also been building. This means that there is a greater probability that economic growth could turn out far worse than current baseline projections. Key risks include the build-up of trade tensions among major economies; increasing geopolitical tensions; greater uncertainty about the path of monetary policy adjustment in developed economies; and high and rising levels of debt in both developed and developing countries. Any of these factors have the potential to derail the recent improvement in economic prospects.

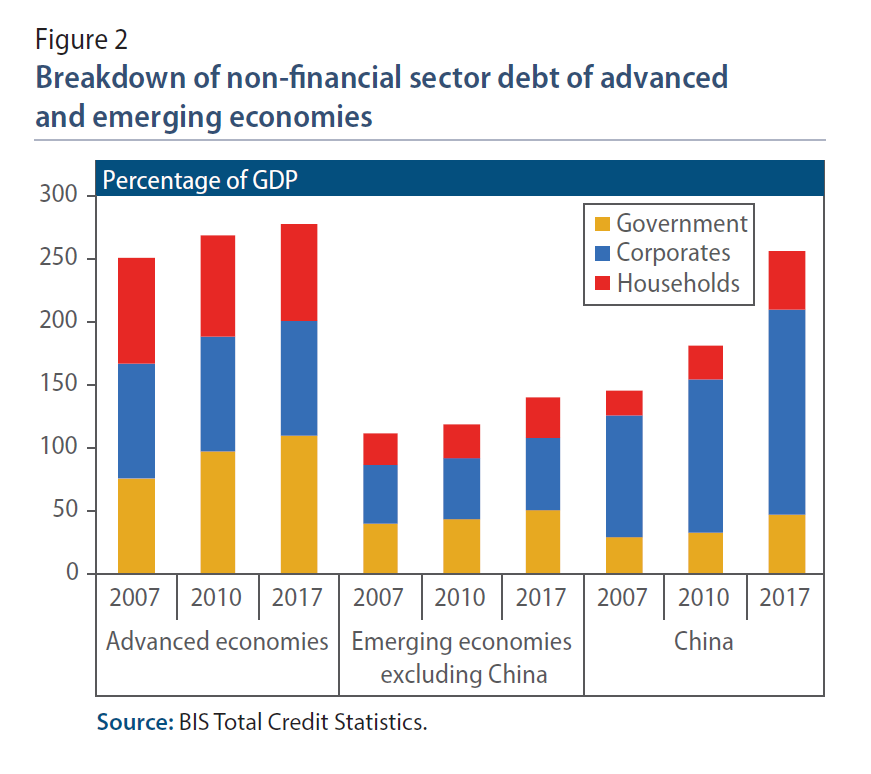

Elevated, and in some cases, still rising levels of debt, is a prominent feature of the global economy. Public and private debt levels remain at historically high levels in many developed economies, and both household and corporate debt is higher than before the global financial crisis. In emerging economies, the debt-to-GDP ratio (all credit to non-financial sector) has increased from 139 per cent in 2010 to nearly 200 per cent in 2017. Non-financial sector debt in China increased from 180 to over 250 per cent of GDP (figure 2). Debt levels in Latin America have also increased visibly, for example in Brazil (from 125 to 145 per cent) and Mexico (from 56 to 77 per cent). In many of these economies, the prolonged period of abundant global liquidity and low borrowing costs has contributed to the “financialization” of the corporate sector. In order to exploit carry trade opportunities, a significant part of corporate debt has been channelled towards real estate and financial assets, rather than productive capital. The extent to which corporate debt is not backed by productive assets poses a source of financial risk.

In response to growing financial risks, policymakers face the challenge of enhancing resilience to external shocks, and in some cases curbing credit growth and managing the pace of private sector deleveraging. If deleveraging occurs too rapidly, it risks triggering a sharp adjustment in asset prices, which may in turn result in elevated banking sector stress and corporate bankruptcies. This process is further complicated by the ongoing adjustment of the monetary stance in developed economies.

In response to growing financial risks, policymakers face the challenge of enhancing resilience to external shocks, and in some cases curbing credit growth and managing the pace of private sector deleveraging. If deleveraging occurs too rapidly, it risks triggering a sharp adjustment in asset prices, which may in turn result in elevated banking sector stress and corporate bankruptcies. This process is further complicated by the ongoing adjustment of the monetary stance in developed economies.

While monetary policy adjustment in developed economies is progressing at a gradual pace, the procyclical nature of fiscal policy in the United States, coupled with potential upward pressure on inflation from proposed import tariffs, has led to increased uncertainty around the pace of adjustment, and raised the probability of a more rapid withdrawal of monetary stimulus. This uncertainty increases the risk of global financial market volatility. Many developing countries are exposed to associated risks, especially where the rise in debt in recent years reflects significant amounts of dollar-denominated debt. The prospects of tighter liquidity conditions and potential spikes in risk aversion expose emerging economies to higher borrowing costs, depreciation of domestic currencies and a decline in equity prices. This could adversely impact banking and corporate sector balance sheets as well as the capacity to roll over debt. Furthermore, the corporate sector will face a heavy debt servicing schedule in the next few years, especially in the case of a sudden appreciation of the dollar. The effects on real economic activity could prove large, through a sharp slowdown in investment, higher inflation or fiscal adjustment measures.

The recent acceleration in economic growth has underscored some of the underlying tensions between economic and environmental targets. CO2 emissions increased by 1.4 per cent in 2017, illustrating that the goal of delinking economic growth from emissions growth remains some way off. The International Energy Agency (IEA), attributes the rise in CO2 emissions to a combination of the acceleration of global economic growth, relatively low cost of fossil fuels and weaker energy efficiency efforts. Improvements in energy efficiency and the pace of energy transition remain inadequate.

According to the International Panel of Climate Change (IPCC), the average global temperature rise will likely range from 4.0°C to 6.1°C relative to pre-industrial levels by 2100 in a scenario of no meaningful action to mitigate GHG emissions growth. It is the stated goal of the Paris Agreement to limit this increase in global average temperature to well below 2°C.

Evidence indicates that in countries with relatively high average temperatures, which include most low-income countries, growth of GDP per capita slows as temperatures rise. Potential channels of transmission include shifting rainfall patterns that may move the locations of arable farmland; rising sea levels, which threaten small island developing States, as well as some of the world’s most valuable coastal infrastructure; and increased frequency and intensity of extreme weather events. Damage through these channels will impact agricultural production, labour productivity in more weather-dependent sectors, capital accumulation and human health, spurring large-scale migrations. Natural disasters already cause the highest numbers of new internal displacements each year: in 2016, new displacements due to disasters were 3.5 times higher than those due to conflict and violence.

Developed economies

United States: Economy near full-capacity

The economy of the United States is operating at or close to full capacity. The unemployment rate has dropped to 3.9 per cent in April 2018, which is below most estimates of its long-run equilibrium level; the ratio of job openings to job seekers is at its highest level since at least 2000; and rising capacity utilization rates have supported a rebound of investment in equipment. While activity moderated slightly in the first quarter of 2018, prospects for the year remain firm, buoyed by major fiscal stimulus measures introduced in the Tax Cuts and Jobs Act of December 2017 and Bipartisan Budget Act of 2018. GDP growth is expected to reach 2.5 per cent in 2018 and 2.3 per cent in 2019. The fiscal stimulus will allow the federal deficit to widen from 3.5 per cent of GDP in 2017 to about 5 per cent by 2019, and government debt will continue to rise relative to GDP for the next decade. The aggressive fiscal expansion, at a point when the economy is operating near full capacity, coupled with potential upward pressure on inflation from import tariffs, may accelerate the pace of interest rate rises by the Fed.

Japan: Recovery continues despite weak first quarter

In the first quarter of 2018, GDP contracted at an annualized rate of 0.6 per cent relative to the previous quarter. The contraction was primarily driven by a rundown in inventories, and prospects for the remainder of the year remain strong. According to the World Economic Situation and Prospects as of mid-2018, the GDP growth forecast for 2018 has been revised upwards from 1.2 per cent to 1.6 per cent, reflecting improvements in both external and domestic demand. Domestic demand is supported by rising corporate profits and tightening labour market conditions. This should support a gradual increase in real wages, which will in turn exert some upward pressure on consumer prices in 2018. The potential for a sharp appreciation of the Japanese yen poses a key downside risk to the economy.

Europe: Solid growth with increased downside risks

The growth outlook for Europe remains robust, but downside risks are high. The euro area is projected to expand by 2.1 per cent this year and 1.9 per cent in 2019, a marginal upward revision compared to forecasts released in December 2017. Strong private consumption growth is underpinned by dynamic labour market conditions and rising disposable incomes. Business investment and construction activity will also be supported by the loose monetary policy stance of the European Central Bank (ECB). However, downside risks to the region’s outlook have increased. Amid rising trade tensions among major economies, various product groups have become the subject of new or changed tariff regimes. A widening of trade restrictions would pose a significant risk, especially to the export-reliant European economies. As the United Kingdom of Great Britain and Northern Ireland prepares to leave the European Union (EU), the transition phase will entail significant uncertainty, particularly over future trade relations between the two parties. This increases the risk of businesses diverting investments away from the United Kingdom. The ECB faces the challenge of designing and communicating a normalization of its monetary policy stance, both in terms of its asset purchases and the policy rate, which could become an additional source of financial market volatility. In Italy, the new government’s stated intentions to move away from euro area-wide agreements could exert significant pressure on the coherence of euro area policy.

Economies in transition

Commonwealth of Independent States: Positive growth maintained; slight downward revision for the Russian economy

The energy-exporting economies of the Commonwealth of Independent States (CIS) are expected to maintain a positive growth trajectory in 2018 and 2019, supported by higher oil prices and prudent macroeconomic policies. The Russian Federation exited recession in 2017, amid stronger private consumption and a moderate rebound in fixed investment, buoyed by preparations for the FIFA 2018 World Cup. In early 2018, low inflationary pressures, a stable domestic currency, and the planned increase in public sector wages laid foundations for a further impetus to consumer spending. However, rising geopolitical tensions followed by additional economic sanctions have subsequently complicated activities of Russian companies and led to a depreciation of the currency. This may spur inflation and curb consumer spending, restraining growth to 1.7 per cent in 2018. In Kazakhstan, growth may exceed 3 per cent, driven by rising oil output and investment in transport infrastructure. Growth is also expected to accelerate in Azerbaijan.

Among the CIS energy-importers, the Ukrainian economy expanded by 2.5 per cent in 2017, supported by a solid upturn in investment. Growth is projected to remain relatively stable in the outlook period, provided external financial assistance continues. Nevertheless, a possible downscaling of the Russian natural gas transit presents a moderate downside risk to growth in 2019. In early 2018, remittance flows to the smaller CIS countries in Central Asia and the Caucasus remained robust, bolstering private spending, although the weakening of the Russian rouble presents a risk. Going forward, the Central Asian countries should also benefit from the implementation of the “Belt and Road” initiative. Aggregate GDP of the CIS and Georgia is expected to increase by 2.1 per cent in 2018 and 2019.

Developing economies

Africa: Growth forecasts revised upward

According to the World Economic Situation and Prospects as of mid-2018, Africa is forecast to grow by 3.6 per cent in 2018 and 3.9 per cent in 2019, marking an upward revision since December. The improvement largely reflects stronger prospects in some of the region’s largest economies—Nigeria and Egypt. Per capita income growth, however, remains very weak, estimated at 1.1–1.3 per cent in 2018–2019, and insufficient to alleviate poverty in the absence of dramatic declines in income inequality. Growth in Nigeria remains subdued, but recent improvement reflects terms-of-trade gains, recovering oil production, greater foreign exchange availability and more solid non-oil growth, driving an upward revision to the forecast for West Africa. North Africa is benefitting from lower inflation in countries such as Egypt and Libya. However, ongoing political instability and security issues continue to hinder prospects for the Libyan economy. Growth prospects have improved for 2018 in East Africa, as continued recovery from droughts and new manufacturing infrastructure spur growth. In Central Africa, fiscal consolidation and lower oil production are projected to constrain growth in 2018. The outlook for Southern Africa remains challenging. However, growth in South Africa is expected to accelerate modestly this year, supported by stronger household consumption and improving investor confidence. Average inflation in Africa remains on a downward trend, reflecting more stable exchange rates and lower food price inflation. This might allow monetary authorities in the region to cut interest rates to support economic activity, especially in East and Southern Africa. However, among the fuel exporters, monetary policy is likely to remain tight. Fiscal deficits should narrow slightly in aggregate, driven by spending cuts and concerns over rising levels of public debt.

East Asia: Growth outlook remains robust but downside risks have increased

The short-term growth outlook for East Asia remains robust, with regional GDP projected to expand at a steady pace of 5.8 per cent in 2018 and 5.7 per cent in 2019. Growth in the region will be underpinned by resilient private consumption and public investment, as well as the ongoing improvement in external demand.

In China, growth is expected to remain solid, supported by robust consumer spending and supportive fiscal policies. While ongoing efforts to address financial vulnerabilities will contribute to more sustainable medium-term growth, the authorities face the policy challenge of ensuring that associated deleveraging does not derail growth in the short term.

Most other economies in the region are expected to experience stable growth in the outlook period. Private consumption will be supported by healthy job creation, low interest rates and modest inflationary pressures. In addition, consumer spending in the Republic of Korea, Myanmar and Thailand will be further boosted by an increase in minimum wages in 2018. Growth in Indonesia, the Philippines and Thailand, will also be supported by large infrastructure projects, which will help to alleviate structural bottlenecks and boost productivity growth in the medium term.

However, downside risks to the region’s growth outlook have increased. A more restrictive global trade environment would significantly impact East Asia, given the region’s high trade openness and extensive global production networks. Meanwhile, geopolitical tensions in the Korean Peninsula could also affect investor sentiments and regional financial markets. In several countries, high corporate debt will continue to weigh on investment prospects.

South Asia: Growth is gaining momentum, but further reforms are needed to promote productivity gains

The macroeconomic outlook in South Asia remains favourable, amid robust domestic demand, strong infrastructure investment and moderately accommodative monetary policies. GDP growth is expected to strengthen to 6.6 per cent in 2018 and 6.8 per cent in 2019, following an expansion of 6.0 per cent in 2017. This positive outlook provides an enabling environment for most countries in the region to make further progress in addressing the vast development challenges across economic, social and environmental dimensions. Deeper reforms, such as strengthening fiscal accounts and tackling the region’s large infrastructure gaps, are also needed to boost productivity gains and unleash the region’s growth potential.

Among the major economies, growth in India is gaining momentum, underpinned by robust private consumption, a slightly more supportive fiscal stance and benefits from past reforms. Although capital spending has shown signs of revival, a more widespread and sustained recovery in private investment remains a crucial challenge. The economic situation in the Islamic Republic of Iran is expected to become more challenging in the near term, due to the re-imposition of trade, investment and financial sanctions by the United States. In addition, structural weaknesses of the Iranian economy due to prolonged periods of under-investment will continue to constrain economic activity in the medium term. Among the smaller economies in the region, Pakistan’s growth is accelerating due to vigorous investment and the gradual recovery of exports. Meanwhile, the Bangladesh economy is set to continue expanding vigorously, amid robust fixed investment and a broadly accommodative monetary policy. The fiscal stance remains prudent, striking a delicate balance between consolidation efforts and advancing large infrastructure projects.

Western Asia: Rising oil prices sustain the economic recovery

The forecast for GDP growth in Western Asia for 2018 has been revised upwards from 2.3 per cent to 3.3 per cent, reflecting a stronger growth projection for Turkey. Economic growth in Turkey accelerated in the second half of 2017, on the strength of recovering domestic demand and stabilising balance-of-payments. Growth in Israel remains robust, with low inflation and strengthening external demand. Meanwhile, the member States of the Gulf Cooperation Council (GCC), namely Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates, are also expanding at a faster pace. The non-oil sector of the GCC countries has been growing steadily, supported by moderate demand growth in the public sector with the recovery in oil revenues. Monetary stances of the GCC countries have been tightened in line with the U.S. Fed. However, financing costs in the GCC countries remain relatively stable, and credit has continued to expand. In Jordan and Lebanon, domestic demand growth remains weak, amid moderate inflation. Fiscal stances in these countries are likely to be tightened as part of reform plans linked to support from international donors. Despite ongoing armed conflicts, more signs of economic stabilisation have been observed in Iraq and Syria. An improvement in the security situation is supporting the Iraqi economy. By contrast, economic recovery in Syria is constrained by its fragile balance-of-payments situation and economic sanctions. The crisis in Yemen remains dire, amid an escalation of conflict, deteriorating food security and deteriorating balance-of-payments conditions.

Latin America and the Caribbean: Economic recovery is projected to gain momentum

Against a backdrop of robust global growth and higher commodity prices, the recovery in Latin America and the Caribbean is expected to gain momentum in 2018–2019. Following growth of 1.0 per cent in 2017, the region is projected to expand by 2.1 per cent in 2018 and 2.5 per cent in 2019. The upturn in economic activity is projected to be broad-based. Except for the Bolivarian Republic of Venezuela, which has entered its fifth year of recession, all countries are expected to record positive growth during the forecast period. The pickup in growth will be driven by strengthening private sector demand, especially in South America’s commodity-exporting countries. Private consumption and investment will be underpinned by modest inflationary pressures, low interest rates and, in some cases, improved confidence. While the easing cycle in countries such as Brazil, Colombia and Peru is expected to come to an end, monetary policy will generally remain accommodative. Moreover, labour markets have shown signs of improvement. In many countries, the unemployment rate has edged lower over the past year, with employment in the manufacturing sector starting to recover. Higher commodity prices and the moderate recovery in growth have helped ease fiscal pressures, particularly in the region’s metals and agricultural exporters. However, in many cases primary balances remain below debt-stabilizing levels, implying a further need for fiscal consolidation.

Despite the projected recovery, Latin America and the Caribbean’s rate of expansion during the forecast period is expected to remain well below the 1991–2012 average of 3.2 per cent. The weak performance of investment and productivity in recent years has raised concerns over a decline in potential growth that could hamper progress towards the SDGs. Moreover, there are significant downside risks to the forecast, including tighter global financial conditions, an escalation of trade tensions and prolonged uncertainty over NAFTA renegotiations. In several countries, economic risks are accompanied by political uncertainties, with key Presidential Elections scheduled to take place in Colombia (May), Mexico (July) and Brazil (October).

Follow Us